(A version of this post also appeared at GigaOM.)

(A version of this post also appeared at GigaOM.)

tl;dr: Cleantech VC is receding because of poor short-term performance – no surprise in a post-bubble field with outsized time and money requirements. The category is about to go on a walk in the woods, where innovators will blaze a new trail.

In late 2011 I decided to write up an internal analysis I’d done at Venrock about the state of cleantech venture capital and make it available broadly. I’m a fact-based, research-driven guy, so I tried to shine the light of data on myths and realities in the field. My macro conclusion was that while it was really early, investment returns to date were on par with VC overall.

Much has changed since then. With 2012 numbers done and dusted, I figure it’s time to revisit this topic – again, under the light of data. I’ll frame this analysis with the questions I’ve gotten from VCs and entrepreneurs who’ve asked me for an update.

What’s happening to cleantech venture capital?

It’s receding.

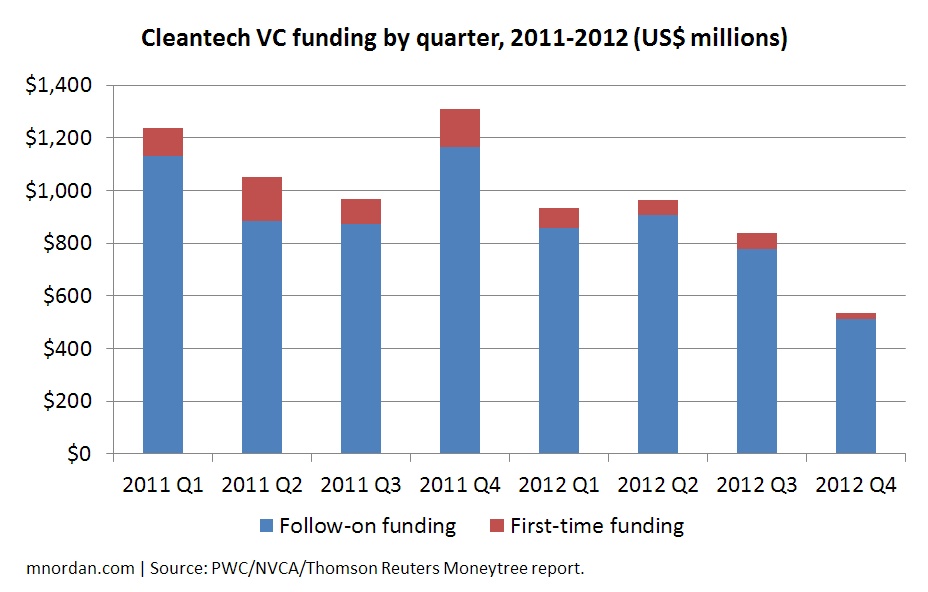

- Investment fell 30% in 2012 – and even further at the early stage. The Moneytree survey numbers had cleantech VC investment falling from $4.6 billion in 2011 to $3.3 billion in 2012 – a 28% drop. Further, they showed first-time funding of new start-ups plummeting 58% to just $216 million, and shrinking as the year progressed: By Q4, first-time funding was just 4% of capital invested.

- Limited partners are backing off. VC firms get the money they invest from limited partners (LPs) like foundations and pension funds. Last December Preqin called up 31 LPs that were invested in at least one cleantech-focused fund and asked if they planned to back any new ones in 2013. Only 22% said yes (down from 31% a year before).

- The people are changing. Many VC firms parted ways with their cleantech teams in 2012. While February’s ARPA-E conference had a record number of attendees, venture investors were scarce – replaced by a bumper crop of corporate types.

Why is this happening?

Cleantech VC performance is substantially lagging venture capital as a whole. This wasn’t true in 2011, but things changed fast in 2012.

I arrive at this conclusion by comparing two data sets. On one hand, we have data on the interim performance of 19 cleantech-only VC funds as reported by the California Public Employees’ Retirement System (CalPERS), a big LP. On the other, we have equivalent data for the entire universe of VC funds from the National Venture Capital Association. (The data are expressed as “value to paid-in capital, net to LPs,” which means “the current value of the funds divided by the money put into them, accounting for what VCs pay themselves.”) By comparing cleantech-only fund performance with the full VC universe at the same points in time, we can see whether cleantech is doing better or worse than the asset class.

The answer is that cleantech went sideways in 2012 while VC overall did well. In September 2010, the cleantech VC funds were worth 0.90x the money paid into them while comparable VC funds overall were at 0.96x – roughly the same. Six months later the gap had widened, but both had risen in value and remained within spitting distance. By June of 2012, however (the most recent data available), the cleantech funds had declined slightly while the overall VC universe climbed to 1.23x.

This is why investment is stalling, LPs are hesitating, and cleantech VCs are thinning: Capital invested in other domains is showing a greater near-term return.

If minimal money had gone into cleantech, or if the macro environment were rosier, there might be more willingness to forge ahead. But today, fund managers assess the $25 billion worth of cleantech VC invested since 2003 against a backdrop of shale gas and climate apathy – and tighten the purse strings.

OK, but why is that happening? What’s driving weak cleantech VC performance?

Two factors. First, there have been too few exits.

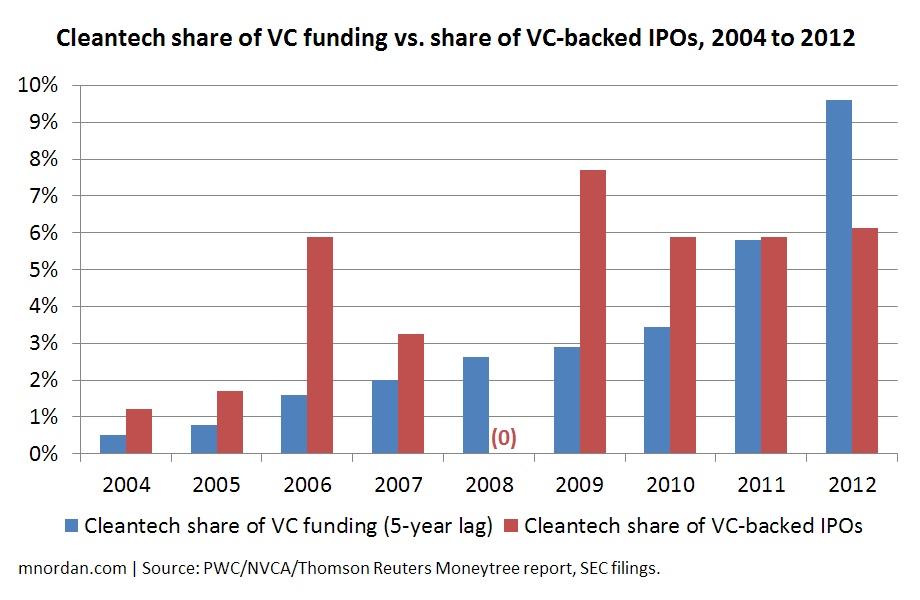

Let’s consider the gold standard of VC wins – an IPO on a major exchange. When I last did this analysis, cleantech was overperforming on the IPO front: In 2009, 2010, and 2011, cleantech’s share of VC-backed IPOs exceeded its share of VC funding. (Note: One must apply an appropriate time lag to the latter – I used five years, which is informed by deal-by-deal fundraising data by cleantech start-ups).

This ended in 2012. Just as in the prior year, three cleantech IPOs took place out of about 50 VC-backed IPOs in total (6%). But cleantech’s corresponding share of VC funding rose to 10% – so cleantech was now underperforming on exits relative to capital invested, instead of overperforming.

(Of course, most VC-backed companies exit through acquisition, not an IPO. But the M&A front looks no better for cleantech. When merchant bank Jane Capital counted up every acquisition of a VC-backed cleantech start-up worth more than $50 million in the last 10 years, it found just 27 of them.)

Second, the winners have disappointed post-IPO. When a start-up goes public, its VC investors rarely get to sell their shares immediately: They have to wait out a lockup period that typically lasts six months. Of the nine VC-backed cleantech start-ups that have done major-market IPOs since 2010 and have been public for more than six months, eight were trading below their IPO price at the 180-day mark.

In four of those cases, the 180-day share price was also lower than the price at the last venture round. That means VCs who bought shares in that round were under water when the lockup expired.

So is the pullback in cleantech VC justified?

Well, it’s certainly expected. The cleantech gold rush of the late 2000s saw hundreds of start-ups funded – many with identical propositions – that greatly exceeded the carrying capacity of their industries: For example, there’s no way that more than a handful of the 219 solar start-ups counted by Greentech Media in 2009 could possibly succeed. This dynamic isn’t unique to cleantech. The Internet VC bubble of the late 90s was the same story, albeit on a much larger scale.

But just as the boom-and-bust in dot com investment didn’t mean this whole Internet thing was a waste, the same is true for energy and environmental technologies. It’s very likely that multiple billion-dollar companies lurk among today’s cleantech VC portfolios. The question is – given the current retrenchment of capital from the field – how many of them will get the fuel to reach the finish line.

In the main, energy and environmental start-ups need outsized time, money, and risk tolerance to reach a big outcome. (That’s not true of IT-meets-energy “cleanweb” companies like Opower or Venrock-backed Nest Labs, but it holds for the deep-tech start-ups that comprise most of the category.) As our case study, let’s take First Solar, the pioneering thin-film solar maker. The company’s first instantiation was founded in 1990; it took 12 years to ship a product, was restarted in 1999, and consumed $150 million of equity investment (all Walton family money) before its 2007 IPO. But at that outcome, First Solar was worth $1.4 billion valuing the Walton stake at 8.4x. Two years later at the peak of the solar boom, it was worth 199x!

If this is what success looks like – that is, if the majority of cleantech start-ups will need more time and money to reach big outcomes compared with VC-backed companies overall – a few conclusions follow:

- Funds focused solely on cleantech will have a longer and deeper “J-curve” of returns compared with VC as a whole. When they reach the same final return multiple, they will take longer to do so (impacting IRR). Midway through the journey, their performance will look like an “L-curve.”

- To the extent that cleantech start-ups’ time to exit will be 10 years or more, it’s too early to call success or failure on the current crop – because most of them were founded in 2007 or later. Check back in five years.

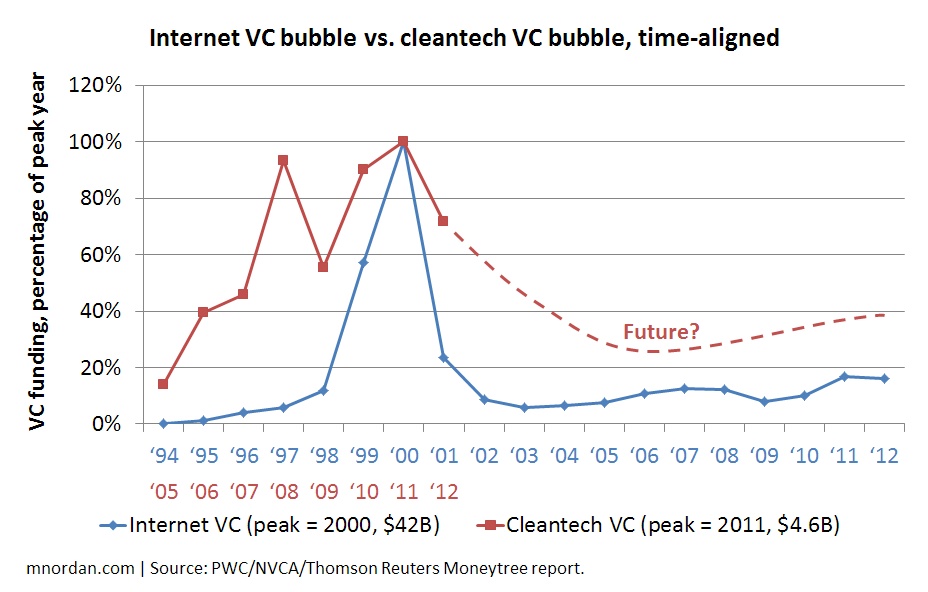

- Because the time frames to an outcome are longer and the amounts of capital required are greater, cleantech investment should be less spikey compared with investment in, say, Internet start-ups. And lo and behold, that’s pretty much what we see:

Cleantech VC now is like Internet VC in 2001: on the downward slope of a bubble, albeit with a more gradual climb and a gentler descent. Note that Facebook was conceived in 2003 – the lowest point for Internet investing post-bust – and that in 2004, Google’s IPO kicked off the renaissance that persists today.

So is the cleantech pullback justified? The data says it’s too early to call. However, it also suggests that the time frame required to reach a conclusion will greatly stretch 10-year closed-ended funds.

(A diligent reader may point out my own numbers showing that when VC-backed cleantech start-ups have gone public, they’ve mostly done so in less than 10 years. My take is that most of these companies were rushed to public markets before they were ready – explaining the awful aftermarket performance.)

What happens now?

Cleantech innovation is about to take a walk in the woods. Justified or not, the established path of VC-backed investment is narrowing for a generation of start-ups. Some of those companies – and some of the investment managers that have backed them – will break off into the wilderness to find a new route.

In this environment, I see opportunities in:

- Selective recaps. About 270 cleantech start-ups can be characterized as “late stage” (they’ve raised Series C rounds or later). Of those, about 150 have demonstrated proof of economics and are focused on scale-up. If capital keeps receding, there won’t be nearly enough money to fund them to exit – enabling savvy late-stage financiers to pick off the best of the bunch in recaps that reap disproportionate returns. In 2011 I thought this capital gap wouldn’t persist, because the likes of VantagePoint and Silver Lake Kraftwerk were out raising huge funds aimed at it; the failure and scale-back of those efforts leaves the opportunity open.

- Cross-border plays. The U.S. dominates cleantech innovation, but China and other overseas nations dominate deployment. New vehicles are mobilizing to provide cleantech equity investment coupled with cross-border JV creation and operational help – including Formation8 and a stealth-mode firm I can’t reveal.

- Strategic investment, rethought. Large corporations in industrials and energy have strategic motivations to foster cleantech start-ups: The likes of GE and General Motors want an innovation pipeline, while utilities want a stream of new equipment to rate-base. Institutions are forming to organize this activity in a merchant banking model, like Broadscale at the late stage and OnRamp Capital at the early.

- Foreign techno-colonialism. While U.S. investors bemoan a lack of capital for cleantech, many foreign institutions are awash in it – and view American assets as being generally cheap. To U.S. start-ups, they will play a role somewhere on a continuum between savior (e.g. Japanese trading houses bankrolling cleantech start-ups to get the inside track on project financing) and reaper (e.g. Wanxiang’s A123Systems deal).

- Philanthropic capital. The cleantech projects that would most change the world – think electrofuels, solar antennae, advanced nuclear power – are also the least likely to be funded, because they combine long time frames with extraordinary risk. There is a case to be made for impact investment in these fields using philanthropic capital as a charitable activity. A new effort called PRIME, backed by four visionary family foundations, is leading this charge.

It’s hard out there for cleantech. The woods are scary and the journey is uncertain. But pioneers are charting a new path through the thicket – blazing trails that others will follow.

I got an outstanding piece of advice in my first job: “Always see the world from the other person’s point of view.”

I got an outstanding piece of advice in my first job: “Always see the world from the other person’s point of view.”

Back in February I acquired a

Back in February I acquired a